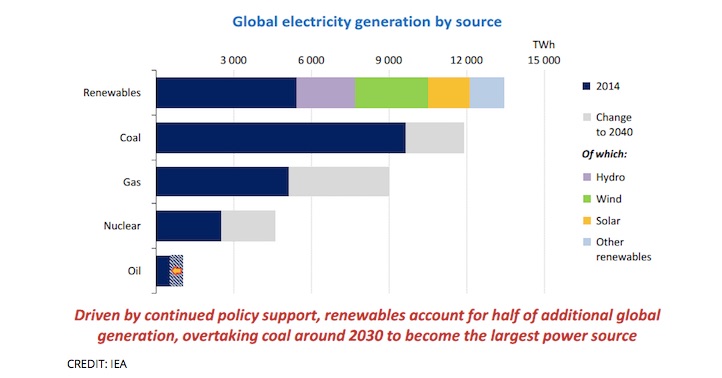

In November, the International Energy Agency quietly dropped this bombshell projection: “Driven by continued policy support, renewables account for half of additional global generation, overtaking coal around 2030 to become the largest power source.” Note 1.

In this post, I’ll dive deeper into this rapidly-approaching role reversal for coal and renewables. In Part Two, I’ll explain why the so-called “intermittency” problem for some renewables is basically solved and thus not a barrier to this reversal.

In releasing its World Energy Outlook 2015 last fall, the IEA published this chart of projected electricity generation in 2040:

The IEA notes, “With 60 cents of every dollar invested in new power plants to 2040 spent on renewable energy technologies, global renewables-based electricity generation increases by some 8,300 TeraWatt-hours (more than half of the increase in total generation).” That increase is “equivalent to the output of all of today’s fossil-fuel generation plants in China, the United States and the European Union combined.” It represents new investment of some $7 trillion in renewables over the next quarter century.

Significantly, this remarkable projection about the future of electricity is simply what the IEA believes is now going to happen given the pledges made in Paris by the world’s leading countries to rapidly expand renewable energy investment while restraining and, in many cases, reducing carbon pollution from fossil fuels through 2030. This is IEA’s “central scenario,” and in it the planet still warms 2.7°C by 2100 and more after that.

In short, this projection is not what would happen if the nations of world pursued the kind of aggressive policies they unanimously agreed to in Paris to avoid very dangerous warming and stay below total warming of 2°C. That would effectively end fossil fuel emissions by 2100.

Indeed, the IEA forecast does not fully take into account what now appears to be an unexpectedly rapid shift away from coal in China. As a result, in its chart, coal power generation increases substantially by 2040. As I reported earlier this month, Goldman Sachs, for one, believes global coal consumption for power generation peaked by in 2013. Note 2.

The IEA itself notes that one of its key assumptions may be too conservative: “China is becoming the wild card of coal markets, with the risks to our projection of a plateau and then a slow decline in coal demand arguably weighted to the downside.” I think the plateau and slow decline scenario was plausible a year ago, but China’s coal consumption dropped nearly 3 percent in 2014, at least 5 percent in 2015, and one analyst in Beijing projected recently, “coal consumption will drop by between 2.5 percent and 3 percent in 2016.” Note 3. Beijing keeps adding new policies to slash coal use, as detailed in a major analysis last month from the Center for American Progress, which concluded “Chinese coal consumption enters downward spiral.” Note 4.

Meanwhile China, the European Union, India, and the United States are speeding up renewable deployment, in many cases faster than expected. Couple that with a likely peak or plateau in global coal use back in 2013, and it’s increasingly clear why renewables will surpass coal to become the primary power source by 2030 even if countries don’t ramp up climate targets any further.

Yet all the worlds’ countries agreed in Paris they would ratchet up their climate targets every five years, which is the only way the world has a chance of staying below the 2°C (3.6°F) defense line — beyond which the risks of catastrophic impacts grow exponentially. If you believe, as I do, that the world is going to seriously attempt to achieve that goal, then we are going to see a lot more renewables relative to coal and even natural gas.

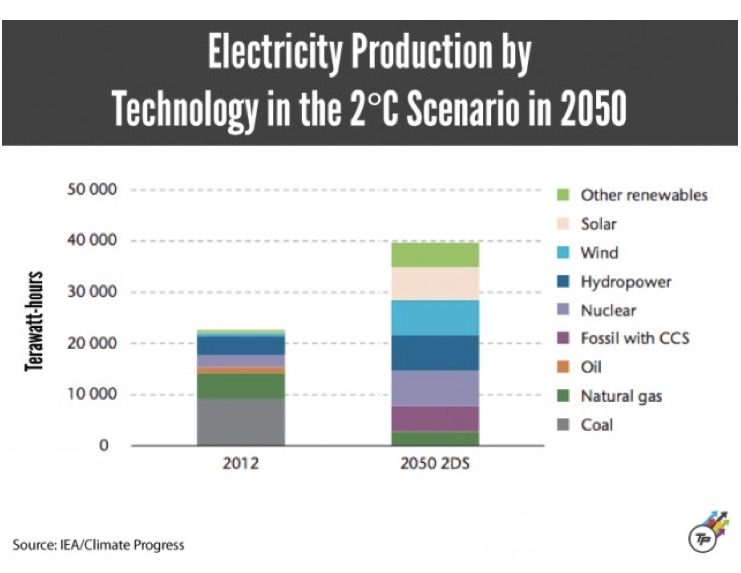

In 2015, the IEA and the Nuclear Energy Agency (NEA) published a technology roadmap for achieving a 2 degrees C scenario (2DS). Note 5. Here is how it breaks down for 2050 compared to 2012:

As you can see, renewables account for the largest share of electricity production globally in 2050 — a remarkable 65 percent. The share of nuclear power rises from 11 percent in 2011 to 17 percent in 2050, which, as I have discussed, is probably the plausible best-case scenario for nuclear. Note 6. We use substantially less natural gas in 2050 than we do today — whatever increase gas might see as a bridge fuel through say 2030 is more than reversed by 2050. And the world has under half the current coal generation, and what coal plants do exist incorporate carbon capture and storage.

This seems like a fairly plausible projection of the future. That’s not surprising, since the IEA is one of the few independent agencies on the planet with an energy and economic model that’s comprehensive and detailed enough to credibly examine in detail the role of various carbon-free technologies in a carbon constrained world.

Significantly, the IEA/NEA scenario has “variable renewables supplying 29% of total global electricity production.” As I’ll discuss in Part Two, contrary to widespread misperception, we already know how to do this through a combination of existing and rapidly-emerging technologies and load-management strategies.

Notes

Note 1. International Energy Agency, World Energy Outlook, 2015 (10 November 2015). www.worldenergyoutlook.org/pressmedia/recentpresentations/151110_WEO2015_presentation.pdf

Note 2. Joe Romm, “We Might Have Finally Seen Peak Coal,” Climate Progress (14 Jan 2016). thinkprogress.org/climate/2016/01/14/3739164/global-coal-peak-2013/

Note 3. Ed King, “Coal, steel sectors to suffer as China pollution drive accelerates,” Climate Home (12 January 2016). www.climatechangenews.com/2016/01/12/coal-steel-sectors-suffer-china-pollution-drive-accelerates/

Note 4. Melanie Hart, “Beijing’s Energy Revolution Is Finally Gaining Serious Momentum,” Center for American Progress (3 Xecember 2015). www.americanprogress.org/issues/security/report/2015/12/03/126606/beijings-energy-revolution-is-finally-gaining-serious-momentum/

Note 5. Nuclear Energy Agency and International Energy Agency, Technology Roadmap 2015. www.iea.org/media/freepublications/technologyroadmaps/TechnologyRoadmapNuclearEnergy.pdf

Note 6. Joe Romm, “Why James Hansen Is Wrong About Nuclear Power,” Climate Progress (7 January 2016). thinkprogress.org/climate/2016/01/07/3736243/nuclear-power-climate-change/

First published in Think Progress/Climate (27 January 2016). thinkprogress.org/climate/2016/01/27/3712181/renewables-surpass-coal-2030/

No comments yet, add your own below